Digital Payments Dominate: 70% of Consumer Transactions by 2026

Anúncios

Anúncios

Digital Payments to Dominate: 70% of Consumer Transactions by 2026

The global economy stands on the precipice of a monumental shift in how consumers conduct transactions. Projections indicate that by 2026, an astounding 70% of all consumer transactions will be facilitated through digital payments. This isn’t merely an incremental change; it represents a fundamental reorientation of financial behavior, driven by technological innovation, evolving consumer expectations, and the relentless pursuit of convenience and efficiency. Understanding the implications of this seismic shift is paramount for businesses, financial institutions, and individuals alike. The rise of digital payments 2026 is not just a forecast; it’s a rapidly unfolding reality.

For decades, cash and traditional card payments held sway, but the digital revolution, accelerated by recent global events, has irrevocably altered the payment landscape. From mobile wallets and contactless cards to online bank transfers and cryptocurrency, the options for digital transactions have proliferated, offering unparalleled speed, security, and accessibility. This comprehensive exploration will delve into the driving forces behind this transformation, examine the technologies enabling it, and analyze the profound impacts it will have on various facets of our lives.

The Irresistible March of Digital Payments 2026: Key Drivers

Several interconnected factors are propelling the exponential growth of digital payments 2026. These drivers are creating a perfect storm, making digital transactions not just an alternative, but often the preferred method for consumers worldwide.

Anúncios

1. Technological Advancements and Ubiquitous Connectivity

The bedrock of the digital payment revolution is continuous technological innovation. High-speed internet, widespread smartphone adoption, and advancements in payment infrastructure have made digital transactions more accessible and reliable than ever before. Near Field Communication (NFC) technology, QR codes, biometrics, and tokenization have streamlined the payment process, making it faster and more secure. The constant evolution of these technologies ensures that digital payment solutions remain at the forefront of convenience.

2. Evolving Consumer Expectations: Convenience and Speed

Modern consumers demand instant gratification and seamless experiences. Waiting in lines, fumbling for cash, or dealing with cumbersome payment processes are increasingly viewed as relics of the past. Digital payments offer unparalleled convenience: a tap, a scan, or a click is often all it takes. This speed and ease of use resonate deeply with a generation accustomed to on-demand services and instant access to information. The expectation for frictionless transactions is a powerful force driving the adoption of digital payments 2026.

3. The Post-Pandemic Push Towards Contactless Solutions

The global pandemic served as a powerful catalyst, accelerating the shift towards digital and contactless payments. Concerns about hygiene and the desire to minimize physical contact propelled many individuals and businesses to embrace digital alternatives. What began as a necessity quickly transformed into a preference, as users discovered the inherent advantages of these methods. This period effectively normalized digital transactions for a vast segment of the population that might have otherwise been slower to adopt.

4. Enhanced Security Features

While initial concerns about digital payment security were prevalent, significant advancements have dramatically improved the safety of these transactions. Encryption, tokenization, multi-factor authentication, and sophisticated fraud detection systems now offer robust protection for consumer data and funds. Many digital payment platforms provide a layer of security that often surpasses traditional payment methods, instilling greater confidence in users and further fueling the growth of digital payments 2026.

5. Financial Inclusion and Accessibility

Digital payments play a crucial role in fostering financial inclusion, particularly in developing economies. For individuals without access to traditional banking services, mobile money and other digital platforms offer a gateway to the formal economy. They enable people to send and receive money, pay bills, and access credit, thereby empowering underserved populations. This aspect of accessibility contributes significantly to the global expansion of digital payment usage.

The Technologies Powering the Digital Payments Revolution

The projected 70% dominance of digital payments 2026 is underpinned by a diverse array of innovative technologies, each contributing to the robustness, security, and user-friendliness of the ecosystem.

1. Mobile Wallets and Payment Apps

Mobile wallets like Apple Pay, Google Pay, and Samsung Pay, along with numerous proprietary bank and merchant apps, are at the forefront of the digital payment surge. These platforms store card details securely, allowing users to make payments with a simple tap or scan using their smartphones. Their integration with loyalty programs and budgeting tools further enhances their appeal.

2. Contactless Card Technology (NFC)

Contactless cards, utilizing Near Field Communication (NFC), allow for quick and secure transactions by simply tapping the card on a compatible reader. This technology offers the familiarity of a physical card with the speed and convenience of a digital interaction, bridging the gap for many consumers transitioning away from traditional swipe or chip-and-PIN methods.

The ease with which consumers can now complete transactions by simply tapping their phones or cards has revolutionized the in-store shopping experience. This frictionless process not only speeds up checkout times but also enhances customer satisfaction, making it a critical component of the growing adoption of digital payments 2026. Businesses that have embraced this technology are seeing tangible benefits, from increased throughput to improved customer loyalty.

3. QR Code Payments

Popular in Asia and rapidly gaining traction globally, QR code payments offer a low-cost and highly accessible digital payment solution. Consumers simply scan a QR code displayed by a merchant using their smartphone camera, confirming the payment via their banking or payment app. This method is particularly beneficial for small businesses and informal economies, as it requires minimal infrastructure.

4. Online Bank Transfers and ACH Payments

While perhaps less flashy than mobile wallets, online bank transfers and Automated Clearing House (ACH) payments remain crucial components of the digital payment landscape. These methods facilitate larger transactions, recurring payments, and business-to-business (B2B) transfers, offering a secure and cost-effective way to move funds digitally.

5. Biometric Authentication

Fingerprint scanning, facial recognition, and iris scanning are increasingly being integrated into digital payment processes to enhance security and convenience. Biometric authentication eliminates the need for passwords or PINs, offering a highly secure and user-friendly method for verifying identity during transactions. This technology is a significant factor in building trust in the digital payment ecosystem and will be integral to the future of digital payments 2026.

6. Blockchain and Cryptocurrency

While still in its nascent stages for mainstream consumer transactions, blockchain technology and cryptocurrencies like Bitcoin and Ethereum offer a decentralized and highly secure alternative to traditional payment systems. As regulatory frameworks evolve and volatility decreases, these technologies could play an increasingly significant role in the long-term future of digital payments, potentially contributing to the growth beyond digital payments 2026.

Implications for Businesses in the Digital Payments Era

The shift towards 70% digital payments by 2026 presents both immense opportunities and significant challenges for businesses across all sectors.

1. The Imperative of Digital Transformation

For businesses, embracing digital payment solutions is no longer optional; it’s a strategic imperative. Merchants must invest in robust point-of-sale (POS) systems that support various digital payment methods, integrate online payment gateways, and ensure a seamless customer experience across all channels. Failure to adapt will result in lost sales and diminished competitiveness.

2. Enhanced Data Analytics and Customer Insights

Digital transactions generate a wealth of data that businesses can leverage to gain deeper insights into consumer spending patterns, preferences, and behaviors. This data can inform marketing strategies, product development, inventory management, and customer relationship management, leading to more personalized experiences and increased profitability. Understanding these insights is key to thriving in the era of digital payments 2026.

3. Reduced Operational Costs and Improved Efficiency

Moving away from cash-based transactions can significantly reduce operational costs associated with cash handling, security, and reconciliation. Digital payments automate many processes, leading to improved efficiency, fewer errors, and faster settlement times. This streamlined approach allows businesses to allocate resources more effectively.

4. Expanded Market Reach

Digital payment platforms break down geographical barriers, enabling businesses to reach a broader customer base, both domestically and internationally. E-commerce platforms integrated with diverse digital payment options allow businesses to tap into global markets, fostering growth and diversification. This global reach is a major benefit for businesses adapting to digital payments 2026.

5. Fraud Prevention and Security Challenges

While digital payments offer enhanced security features, businesses must remain vigilant against evolving cyber threats and fraud attempts. Investing in advanced fraud detection systems, complying with payment card industry (PCI) data security standards, and educating employees on best practices are crucial to protecting both the business and its customers.

Impacts on Consumers in the Digital Payments Landscape

Consumers are at the heart of this transformation, experiencing both the benefits and potential pitfalls of a predominantly digital payment world.

1. Unprecedented Convenience and Accessibility

For consumers, the primary benefit of digital payments is unparalleled convenience. The ability to pay quickly and securely, whether online, in-store, or peer-to-peer, simplifies daily life. Access to financial services becomes easier, especially for those in remote areas or without traditional bank accounts. This ease of use is a core driver for the rapid adoption of digital payments 2026.

2. Enhanced Financial Management

Many digital payment apps and platforms offer integrated budgeting tools, transaction tracking, and spending insights. This allows consumers to gain a clearer picture of their financial habits, helping them manage their money more effectively and achieve financial goals. The transparency offered by digital records is a significant advantage.

3. Loyalty Programs and Rewards

Digital payment platforms often integrate seamlessly with loyalty programs, offering consumers rewards, discounts, and personalized offers. This creates an incentive for continued digital payment adoption and fosters stronger relationships between consumers and their preferred brands. These incentives are powerful motivators for consumers to use digital payments 2026.

4. Privacy Concerns and Data Security

While security measures are robust, consumers still face privacy concerns regarding the vast amounts of data collected through digital transactions. Understanding how their data is used and ensuring platforms adhere to strict privacy regulations are critical for maintaining consumer trust. Educating consumers about data protection is vital.

5. The Risk of Digital Divide

As digital payments become the norm, there is a risk of excluding individuals who lack access to smartphones, internet connectivity, or the digital literacy required to navigate these systems. Efforts must be made to ensure that the transition is inclusive, providing alternatives or support for those who may be left behind in the race towards digital payments 2026.

The Global Perspective: Regional Variations and Growth

The pace and nature of digital payment adoption vary significantly across different regions of the world, influenced by economic development, regulatory environments, and cultural factors.

1. Asia-Pacific Leading the Charge

The Asia-Pacific region, particularly countries like China and India, has been at the forefront of the digital payment revolution. Mobile wallets and QR code payments are ubiquitous, driven by large tech companies and a young, digitally native population. This region provides a glimpse into the future of digital payments 2026 for the rest of the world.

2. Europe and North America: Catching Up Rapidly

While initially slower to adopt, Europe and North America are rapidly catching up, driven by increased contactless card usage, the proliferation of mobile wallets, and the rise of fintech innovations. Regulatory initiatives like PSD2 in Europe have also spurred innovation and competition in the payment sector.

3. Latin America and Africa: Leapfrogging Traditional Banking

In many parts of Latin America and Africa, digital payments are enabling populations to leapfrog traditional banking infrastructure. Mobile money services have become essential for remittances, everyday transactions, and financial inclusion, empowering millions who were previously unbanked. The growth in these regions is expected to contribute significantly to the 70% target for digital payments 2026.

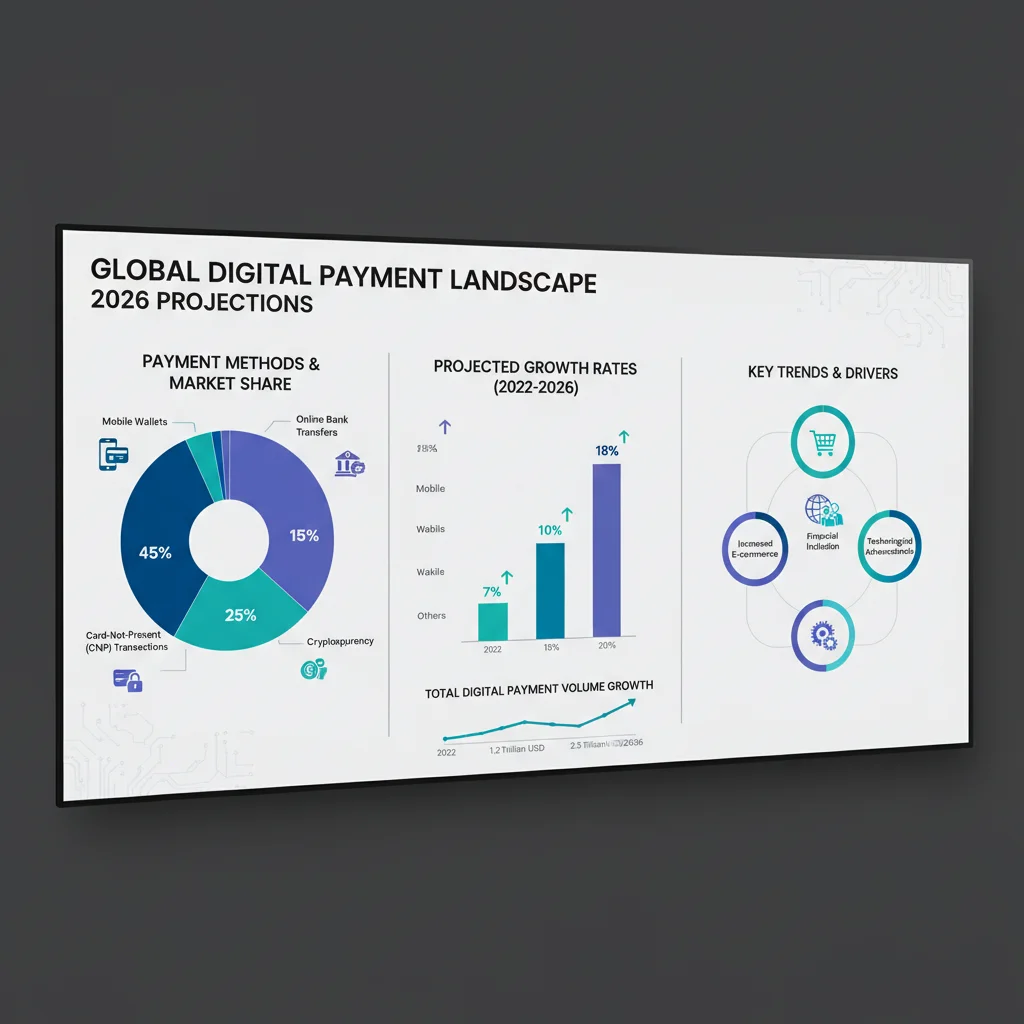

The infographic above clearly illustrates the projected market landscape for various digital payment methods. It underscores that while mobile wallets are expected to capture a significant share, other forms like online bank transfers and card-not-present transactions will also see substantial growth. This diversification of digital payment channels ensures resilience and caters to a wider range of consumer and business needs, reinforcing the forecast for digital payments 2026.

Preparing for a 70% Digital Payment World

As the deadline of 2026 rapidly approaches, stakeholders must actively prepare for a world where digital payments are the dominant transaction method.

For Businesses:

- Invest in Omnichannel Payment Solutions: Ensure seamless payment experiences across online, mobile, and in-store channels.

- Prioritize Security: Implement robust cybersecurity measures and adhere to compliance standards to protect customer data.

- Leverage Data: Utilize transaction data to personalize customer experiences and optimize business operations.

- Educate and Train Staff: Equip employees with the knowledge and tools to handle various digital payment methods and assist customers.

- Explore New Technologies: Stay abreast of emerging payment technologies like blockchain and AI-driven fraud detection.

For Consumers:

- Embrace Digital Wallets: Familiarize yourself with mobile payment apps and contactless card usage for convenience and security.

- Monitor Your Transactions: Regularly check bank statements and payment app histories for any suspicious activity.

- Understand Privacy Settings: Be aware of how your data is being used and manage privacy settings on payment platforms.

- Stay Informed: Keep up-to-date with new payment technologies and security best practices.

For Financial Institutions and Regulators:

- Foster Innovation: Support the development of secure and efficient digital payment infrastructures.

- Ensure Regulatory Clarity: Develop clear and adaptable regulatory frameworks that promote innovation while safeguarding consumers.

- Address Financial Inclusion: Implement policies and initiatives to ensure that digital payment adoption is inclusive and leaves no one behind.

- Strengthen Cybersecurity Defenses: Collaborate to build a resilient and secure digital financial ecosystem.

Conclusion: The Future is Frictionless and Digital

The projection that 70% of consumer transactions will be digital by 2026 is not just a statistical forecast; it’s a profound indicator of a global transformation in financial behavior. The convergence of technological innovation, evolving consumer demands, and a heightened awareness of efficiency and security has set the stage for this dramatic shift. Businesses that embrace this change, adapt their strategies, and prioritize customer experience will be well-positioned to thrive in the new digital economy. Consumers, in turn, will benefit from unparalleled convenience, greater control over their finances, and access to a wider array of services.

While challenges remain, particularly around security, privacy, and inclusivity, the trajectory towards a predominantly digital payment landscape is irreversible. The future of commerce is frictionless, interconnected, and overwhelmingly digital. The era of digital payments 2026 is upon us, and understanding its nuances is key to navigating the next chapter of global finance.